Published 25-12-2014, 08:41

Federico Pieraccini

.

There are two central issues related to the devaluation of the ruble and the dollar depreciation to keep in mind: the preservation of American hegemony and the speculative bubble of derivatives linked to industry of Shale Gas. Without these elements, it is impossible to understand what are the reasons and the consequences of these artificial economic actions.

This case must therefore necessarily be addressed from different perspectives, a geopolitical one and a purely economic one.

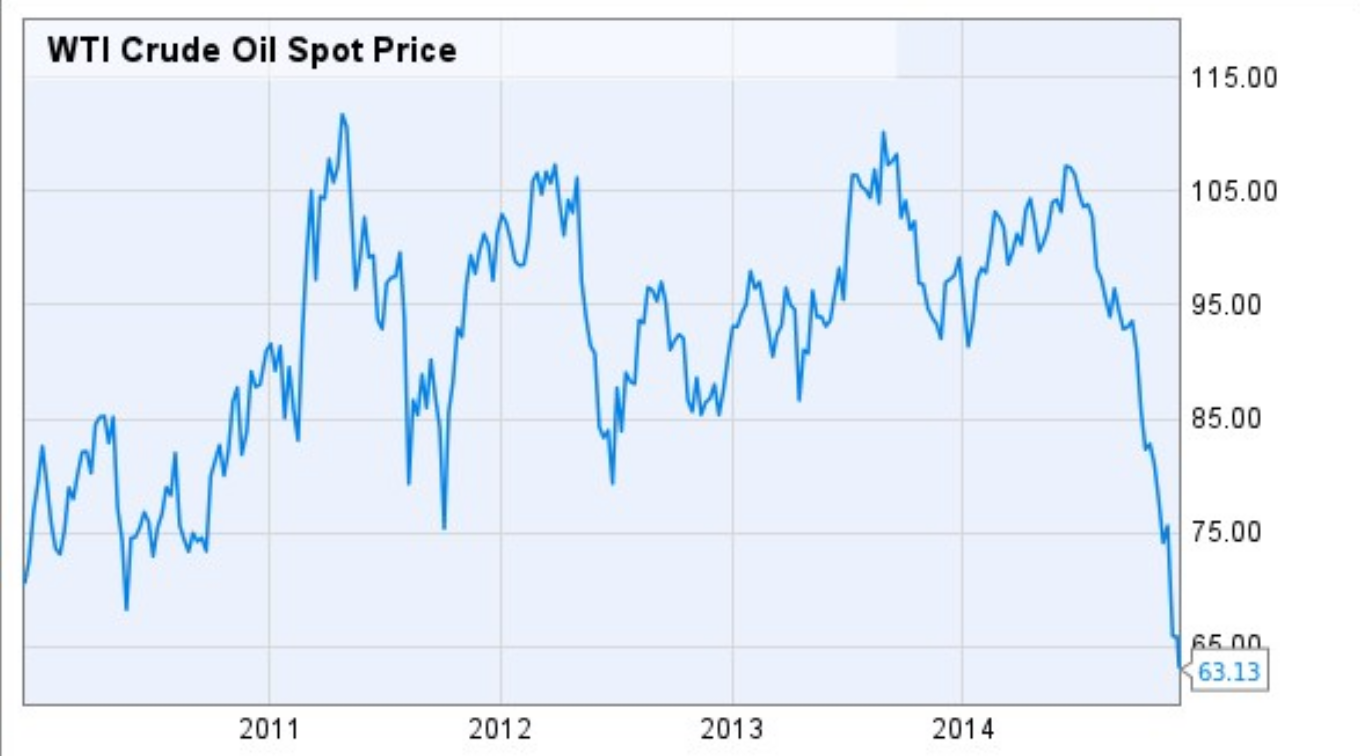

The collapse of oil.

The depreciation of oil seems to be a strategy implemented by mutual agreements between the US State Department and the Royal House of Saudi. As you can read in the article, the meetings in September 2014, between Kerry and Prince Abdullah laid the foundations for a decline in crude oil prices (compared to the market value) and at the same time a denial in the reduction of daily production. An artificial manipulation of oil prices in all means. This seems to be the central reason why, despite a collapse inside the stock market in the UAE (losses between 8% and 20% in a single day on the 16th of December), there aren’t any short-term intentions to decrease the daily output of oil production.

The immediate effects of this situation are tangible in countries where the break-even point ("The break-even point is a value that indicates the amount, expressed in volume production and sales, product sales required to cover the costs previously incurred, in order to close the reference period without profits or losses.") for extraction of crude oil varies over 90$ a barrel. From Iran to Venezuela, passing through Russia, all these countries are affected by the collapse in the value of crude oil. Riyadh is less effected, since it’s break-even point is around 65$.

It's a situation that for some countries is not sustainable for much longer, of course we are not speaking about Russia that has a good economic base (low debt, high gold reserves, much foreign currency liquidity), but rather about countries like Venezuela ( break even in a range 140-160$) which receive much of their income from gains on oil export. Combining this situation with the sanctions imposed on Caracas and we could be facing an economic collapse in Venezuela (Zero Hedge has placed at 93% the chance of a default ). Not to mention that even the Iranian oil is affected by these declines (break-even between 120- 140$), with great satisfaction of Riyadh, the regional competitor.

Flood the market with something that has a very low demand ( are we at the peak for demand of oil ?) and what you get is deflation and this is tangible even to the less attentive observers. If the world economy slows, thus also the need of energy will fall contextually. If this decline is not matched by a decrease in production (as required at OPEC two weeks ago), then the price will collapse to the current value. In a sense, the ordinary citizen could argue that the price per barrel today is much more in line with market values at this stage of the global economy .Unfortunately, it is only one of many points of view from which to observe this scenario and certainly does not offer a complete explanation.

The depreciation of the ruble

Undoubtedly there is a strong correlation between the fall in crude oil prices and the collapse in the value of the ruble. But this theory does not offer a sufficient explanation. There are other factors that cannot be ignored.

The economic sanctions imposed by the United States and the European Union prevent lending to Russian companies, with payment terms beyond 30 days. Given that Russian companies get cheap money from the West banks since the end of the Cold War, the sanctions currently prevent a restructuring of previous loans and refinancing more of the same. The consequences are that these companies must now buy Euros and Dollars to take care of their loans, thus creating more demand for foreign currency in the Russian market and thus weakening the ruble. From a purely business point of view, the Russian companies would like to see a different behavior of the Russian central bank, as explained by Alexander Mercourius:

"What I suspect, about what is happening, is that major speculators against the ruble are just the banks and Russian companies that have a large amount of dollar loans to be repaid before the end of the year. Instead of paying these debts with their reserves, they are putting pressure on the government and the central bank converting rubles into dollars and speculating against the ruble. And this aspect is much more important than any other factor that caused the recent defeat of the ruble. Judging from what Ulyukaev says, the government and the Central Bank have essentially capitulated and decided to help banks by giving them some of the reserves of the Central Bank. This may explain why the rate increase on the 15th of December was so ineffective and why in the last days the ruble has strengthened."

Indeed analyzing the side effects of the Bond issued by Rosfnet on December 12th, 2014 (625 billion rubles - amounting to 11 billion dollars to 15/12), it seems that in the end the Russian central bank bought this bond, letting Rosfnet refinance loans, with Western banks. One could argue that the United States applies the same tactics using the Fed to simply print money and give them out to American business in trouble, in change of bond emissions. The behavior of the Russian central bank, similar to the Fed’s, has been an obligated one. The problem is that the global system is calibrated on the Dollar, not on the ruble. Russia used a Western method to create money and pays the consequences. These same consequences are the mother of all frightens for Americans with the process of De-Dollarization and the Dollar losing credibility.

The geo-political factor of this crisis

"We could of never imagineed what is happening, it is the materialization of our worst nightmares. And in the next few days I think the situation could be comparable to the most difficult period of 2008 " - Sergei Shvetsov, First Deputy Governor of the Central Bank of Russia.

The most interesting question to ask is: could of the Russian authorities predict this combined attack oil-ruble-sanctions? The answer is yes and they did. Too bad no one could of imagined a so immediate acceleration of this strategy. Not even in the deepest nightmares of the Russians, in 6 months, the oil would be reduced to half of its value and the ruble of more than 50% in 12 months. This American tactic requires an extremely high risk factor and that endangers the 'entire global economy, as we shall see .

Why then have the United States and its partners come to take this path so full of unknowns? Even in this case there are multiple answers. Certainly the main thrust concerns the geopolitical strategy of 'regime-change' in countries such as Venezuela, Iran and Russia ( in fact the most affected by the collapse of the price of oil). If using normal methods of softpower obtained not very significant results (Iran is heading to the agreement 5 + 1, Assad is increasingly solid in Syria, Putin is becoming increasingly popular at home and Maduro was able to regain the reins of the country after a period of instability following the death of Chavez and the artificial protests in the summer), in this way the key is an economic leverage. Never the less, there are many risks in this strategy. The collapse of the currency, the decrease in revenues from crude oil, rising prices, rising inflation, declining purchasing power and so on are the weapon with which America is convinced that it can continue its role as a hegemon in the world. The order is to lead to a collapse of domestic rival nations thanks to a combination of factors: sanctions, oil and currency.

What are the risks of this strategy?

After analyzing the motives and methods used to pursue this Kamikaze strategy, we can analyze certainly a more interesting but also more disturbing issue: the risks that these methods implemented by the west could trigger. The crisis in Ukraine, the Eurasian Union, the de-dollarization and the mega agreements between BRICS countries led to a backlash in Washington, with a game of risking everything.

The factor that carries the major unknowns but also the major concern is the market of the Shale Gas in America. Raised as a banner of American energy independence, coveted as a weapon to transit from the Middle East towards Asia (part of the strategy of "Asian Pivot"), it has undeniably played (and still plays) a primary role in the plans of policy makers in Washington.

Yet what is cleverly concealed by the mainstream media are the side effects that the market of shale gas suffers at the current low oil prices. The break-even point for these new methods of extraction is between a range of 60-80$ per barrel. Given this, it is easy to understand that with a prolonged period of low prices, the effects will be devastating for the whole market of Shale gas in the US (the first case of this kind has already happened, the Red Fork Energy Australia yesterday went into controlled administration ). If these were the only consequences, we could simply consider them irrelevant. The problem comes when we focus on the lending process to these companies that fail to return the credits to banks if they go bankrupt. A default in this industry sector could trigger a cascade mechanism which would ultimately affect the mother of all bubbles: the derivatives well hidden in Western banks.

The big global risk that the United States are taking to maintain their global hegemony is not much different from a preemptive nuclear attack (seems a doctrine of first strike in an economic sense). If the price of oil (artificially manipulated) drags into the abyss the Shale Gas Industry of America, all loans that should be repaid to the US banks would go in smoke. With them, potentially, all the derivatives:

Let’s give some the numbers to these words and see how many of these crazy financial instruments, the US banks have:

JPMorgan Chase

- Total Assets: $ 2,520,336,000,000 (about 2.5 trillion dollars)

- The total exposure to derivatives: $ 68,326,075,000,000 (more than 68 trillion dollars)

Citibank

- Total Assets: $ 1,909,715,000,000 (just over 1.9 trillion dollars)

- The total exposure to derivatives: $ 61,753,462,000,000 (more than 61 trillion dollars)

Goldman Sachs

- Total Assets: $ 860,008,000 (less than a trillion dollars)

- The total exposure to derivatives: $ 57,695,156,000,000 (more than 57 trillion dollars)

Bank Of America

- Total Assets: $ 2,172,001,000,000 (a little 'more than 2.1 trillion dollars)

- The total exposure to derivatives: $ 55,472,434,000,000 (more than 55 trillion dollars)

Morgan Stanley

- Total Assets: $ 826.568 billion (less than a trillion dollars)

- The total exposure to derivatives: $ 44,134,518,000,000 (more than 44 trillion dollars)

A useful comparison to fully realize what numbers we're talking about: the US public debt amounts to 18 trillion dollars. The derivatives markets, only of the six largest banks in America, amounts to almost 16 times the US debt!

We are faced with yet the same dilemma already of the 2008 financial crisis: let banks fail or save them? Can the banks fail or are they "to big to fail”? In this case there are two possible ways: Print money (the Feds way of solving every problem) without worry of the increasing public debt (the example used so sustain this theory is Japan with 300% of debt) or let banks fail.

Taking for granted that the manipulation of the oil market and consequently the ruble affair are geopolitical moves, then what is the winning strategy that Washington hopes to obtain, without causing a collapse of the global economy? Foster a regime change in Venezuela, Iran and Russia in a short time or compel these nations to come to terms with the dictates of the West. It's important to note that the time is NOT on the side of the West. The reason is related to the arguments set out above: an oil price so low would send down the drain the market of Shale gas, causing a chain reaction that would destroy the major US banks and could trigger the biggest speculative bubble in human history, the derivatives, which would cause an economic crisis in the face of which what happened in 2008 would be remembered as something easy.

There is one factor that matters more than any other and is considered by the US as the real key to this strategy. If the market of the Shale came to collapse and US banks have to be saved again ( as they are asking the government since December 11th ), the solution would be to simply print more money from the Fed and increase the US public debt. One might object that this would decrease significantly the credibility of the dollar itself. It's a matter of debate and no one has a definite answer. Surely in the US, they are convinced that if this tactic would be successful and lead to a regime change and economic collapse of Russia, China would be forced to "return to the fold" (having lost here number 1 ally), thus ensuring the good solidity of US Treasury (the credibility of the dollar is very dependent on China because of the amount of American Treasury Bonds detained by the Chinese) and confirming the credibility of the dollar itself (even in a situation where the public debt were to move from 16 to 36 trillion dollars).

The basic problem remains geopolitical. The hegemonic view that the US need and want to keep . They currently have no other means to fight a global change that is transiting humanity in a stage no longer unipolar (in which the Americans is the only super-power) but multipolar (more actors on the world stage). We are reckoning and current drift presents an incalculable risk for the entire global economy ... it really worth it?

_jpg/250px-ElbeDay1945_(NARA_ww2-121).jpg)